This post first appeared on Risk Management Magazine. Read the original article.

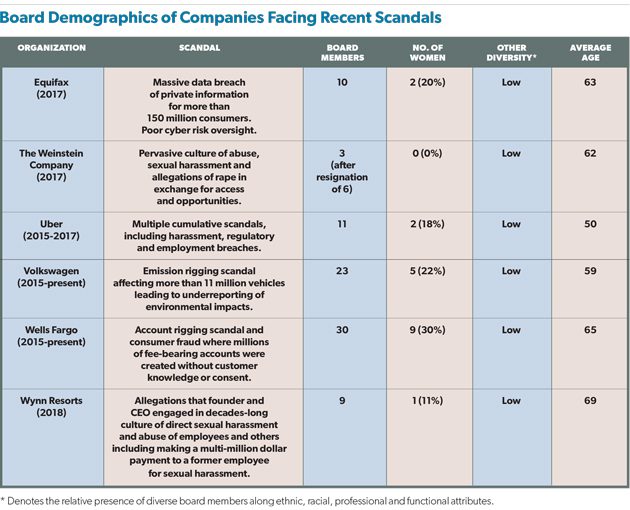

On the surface, the circumstances surrounding scandals faced by Equifax, Wells Fargo, The Weinstein Company, Uber, Volkswagen, Wynn Resorts and others could not seem any more different. Upon deeper analysis, however, a common thread in each of these cases could offer insight for companies to avoid future problems: At the time of these corporate failures, the board of each company lacked diversity and was unable or unwilling to fully understand the gamut of their non-financial environmental, social and governance (ESG) issues, risks and opportunities.

The Connection Between Diversity, ESG and Profitability

Recent research has underscored the strong relationship that exists between diversity among leadership and ethical behavior, and superior resilience and long-term profitable sustainability. For example, the January 2018 McKinsey & Company report Delivering Through Diversity found a continuing strong link between diversity and performance. Companies in the top quartile for gender diversity on their executive teams were 21% more likely to have above-average profitability than companies in the fourth quartile. In terms of ethnic and cultural diversity, top-quartile companies were 33% more likely to outperform their peers on profitability. These trends were true at the board level as well. “We found that companies with the most ethnically/culturally diverse boards worldwide are 43% more likely to experience higher profits,” McKinsey wrote. “We also found a positive correlation between ethnic/cultural diversity and value creation at both the executive team and board levels.”

In their 2017 research on “total societal impact,” Boston Consulting Group (BCG) also made the business case that for-profit companies that place greater emphasis on ESG measures can improve their valuations and margins. In addition, the Ethisphere Institute tracked the stock value of publicly traded companies on its annual Ethisphere Most Ethical Companies list and found that companies with robust ethics and compliance programs experience what they call an “ethics premium.” Over a three-year period, their stock value was 4.88% higher on average than that of companies without such programs.

The importance of diversity and ESG issues has not been lost on business leaders. For example, the National Association of Corporate Directors’ Blue Ribbon Commission Report on Culture as a Corporate Asset acknowledges the impact corporate culture can have on organizational performance and reputation. It also provides recommendations for boards to assess the health of their corporate culture and ensure that such an ethos is embedded in strategic discussions and driving the right behaviors.

In addition, Larry Fink, chairman and CEO of BlackRock, the world’s largest asset management firm, wrote in his 2018 letter to CEOs that the company will continue to emphasize the importance of a diverse board. “Boards with a diverse mix of genders, ethnicities, career experiences, and ways of thinking have, as a result, a more diverse and aware mindset,” he wrote. “They are less likely to succumb to groupthink or miss new threats to a company’s business model. And they are better able to identify opportunities that promote long-term growth.”

If the boards of Wells Fargo, Uber, Volkswagen, Equifax, Wynn and The Weinstein Company had been significantly more diverse, perhaps they would have had more risk resilience programs in place and fewer of these cases would have exploded into scandals. This is because more diverse boards are better at understanding, overseeing and balancing not only financial issues but ESG issues as well. Unfortunately, the boards of far too many companies are still too “pale, stale and male,” populated by current or former CEOs and CFOs, and often devoid of any notable expertise in ESG and risk governance. Governance diversity means being inclusive of those who are most relevant to the business of a company—from both a financial, operational and an ESG standpoint—whether that diversity relates to gender, ethnicity, race, nationality, age, functional or professional expertise, or leadership qualities.

If the boards of Wells Fargo, Uber, Volkswagen, Equifax, Wynn and The Weinstein Company had been significantly more diverse, perhaps they would have had more risk resilience programs in place and fewer of these cases would have exploded into scandals. This is because more diverse boards are better at understanding, overseeing and balancing not only financial issues but ESG issues as well. Unfortunately, the boards of far too many companies are still too “pale, stale and male,” populated by current or former CEOs and CFOs, and often devoid of any notable expertise in ESG and risk governance. Governance diversity means being inclusive of those who are most relevant to the business of a company—from both a financial, operational and an ESG standpoint—whether that diversity relates to gender, ethnicity, race, nationality, age, functional or professional expertise, or leadership qualities.

Most boards are 85% dominated by men, have an average age of 62 or over, and exhibit low levels of diversity in ethnic, racial, professional, and functional attributes. The reality is that most boards exclude women, people of color, younger professionals, and global and non-financial business experts. In defense of their staid ways, many boards claim to be “diverse in thought,” suggesting that, despite their homogenous backgrounds, they still are able to contribute a wide range of viewpoints and ideas. While this may be true in some cases, the bottom line is that since most boards continue to be almost entirely made up of the same narrow candidate pool, their primary focus is still on growth, profits and maintaining status quo. Worse still, many boards are composed of friends and family of the CEO who are often loath to challenge existing strategies and processes and are subject to paycheck persuasion.

Leadership and Culture

While this may be changing, albeit slowly, a review of the world of business and governance reveals that there is still much progress to be made on board diversity, especially in the United States where there are no board gender quotas as there are in many European countries. The argument still used today to justify low levels of diversity is that there is a “lack of suitable talent,” but all too often this is subtle prejudice masked as meritocracy. Meanwhile, the “diversity of thought” claim many companies and their boards make is often just a cop-out for instilling real diversity of background and experience. Many boards have become parochial in thought, judgment and action. The lack of meaningful commitments to diversity that reflects society, markets, investors and other stakeholders is harming private enterprise.

Recent corporate scandals have resulted in billions of dollars in lost market value, not to mention ongoing financial, reputational and legal consequences. In many such cases, CEOs are let go gently with golden parachutes while boards remain largely intact and in place, even amid questions about the apparent lack of appropriate response to ongoing concerns within the company.

There are two common and deeply interrelated threads running through these scandals. First, there was the breakdown or complete lack of appropriate risk oversight at the board level, especially relating to leadership and culture—the two most important strategic risks for which the board is uniquely responsible. Second, there was a prevailing homogeneity of background, expertise and demographics of individual board members, leading to “groupthink” that likely exacerbated these problems.

Research shows that more diverse boards and executive teams deliver greater financial value and engage in more successful strategic decision-making. Many companies are getting this equation right, understanding that in order to remain sustainable, profitable and attractive for long-term investment, they must pay attention to more than just traditional financial factors. They have come to realize that good ESG management, including diversity and inclusion within their employee population, management and board, is also good for business.

Beyond the Status Quo

The role of the board is not only to challenge management to achieve financial results but to achieve them in a manner congruent with stakeholder trust and value systems. In a market where trust is the most important asset organizations have, the board must be the sentinel of that institutional trust. This responsibility is perhaps a taller order than what many board members signed up for, but it is the best way to preserve enterprise value, guard against complex risk and retain stakeholder trust.

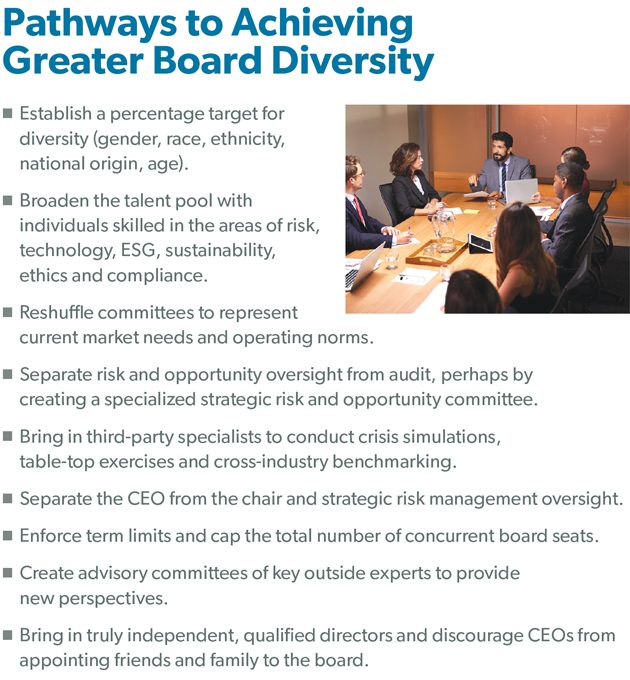

We are living at a time of unprecedented global risk due to the convergence of serious and rapidly scaling challenges, disruptions and potentially existential threats, from technological innovation and disruption, climate change, geopolitical instability, the severe decline of trust in all institutions, and the attendant acceleration and amplification of reputation risk by social media. In this rapidly changing world, companies need to have boards that are agile enough to keep pace with these new and emerging challenges. Boards must move from a position of sitting back to leaning in when it comes to promoting the diversity of people, backgrounds and expertise among decision-makers.

All too often, large enterprises have no notable separation of powers when it comes to the chairman and CEO roles, which are most often held by a single person, usually a man. Additionally, there is no demonstrable independence when it comes to risk oversight and corporate governance standards. As a result, many boards avoid decisions and essentially become a rubber stamp for the status quo. Stubbornly adhering to such a limited perspective can create severe blind spots and ultimately destroy corporate value. Challenging conventional board structures with more diverse candidates can help the board to consider different perspectives, ask a different set of questions about company strategy, and act as the necessary third rail that keeps management in check.

Boards have a crucial role to play in guiding not only financial returns but ESG impacts. A dramatic shift is taking place in governance for the dual purpose of maximizing financial returns and creating common social good for the broader stakeholder community. The role of the board must evolve beyond check-the-box compliance and move to embrace a holistic and integrated strategic oversight of ESG, enterprise risk management, leadership and culture. An essential part of achieving this objective is to have a properly diversified board.